The Chamber of Commerce of Spain predicts that the Spanish economy will grow by 2.3% in 2026 if the Strait of Hormuz is unlocked, but it also considers two more negative scenarios if the conflict prolongs.

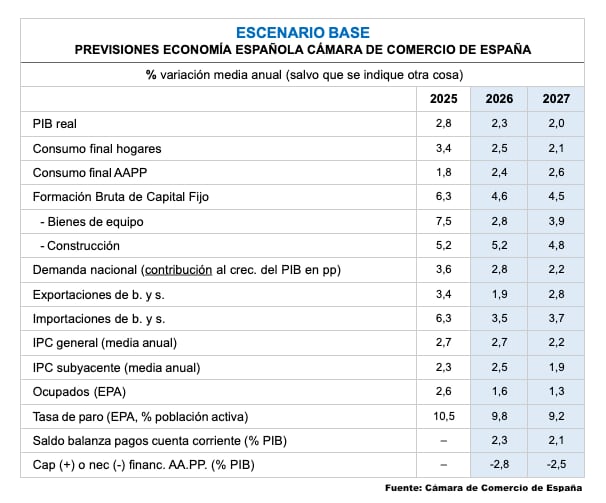

The Spanish economy will maintain its growth path in 2026 and 2027, with a GDP increase of 2.3% in 2026 and 2% in 2027, according to forecasts released by the Chamber of Spain. This projection is mainly supported by the strength of domestic demand, thanks to the dynamism of consumption and job creation.

This forecast, according to the Chamber in a press release, has been established under the hypothesis that the interruption of maritime traffic in the Strait of Hormuz, a mandatory passage for 20% of the world’s crude oil and 25% of liquefied natural gas, will be temporary and the military conflict will be resolved in a matter of weeks. However, inflation may not drop below an average of 2.7% during 2026, before moderating throughout 2027.

The labor market would maintain a very positive evolution, with the creation of 360,000 jobs in 2026 and nearly 300,000 in 2027, and a gradual reduction of the unemployment rate to 9.2% in 2027.

As for investment, it could continue to grow in the coming years, although with more prominence from construction, which would advance by 5.2% in 2026 and 4.8% in 2027, compared to the more moderate growth of capital goods and intellectual property (2.8% and 3.9%).

An evolution that reflects the uncertainty of the moment and also the end of the boost from the NextGenerationEU funds, although in 2027 the effect of projects that are already underway will be noticeable.

Domestic demand will continue to be the engine of the economy, contributing 2.8 points to GDP in 2026 and 2.2 points in 2027.

On the contrary, the external sector will detract from growth, due to weaker international demand. Exports will barely grow by 1.9% in 2026, rising to 2.8% in 2027, while import growth will be higher —3.5% in 2026 and 3.7% in 2027— driven by the strength of consumption.

These estimates, however, are subject to numerous uncertainties, given the extreme volatility in the geopolitical situation. Therefore, the Chamber of Spain has projected two other scenarios under the hypothesis of a longer duration of the conflict.

These scenarios allow for a more precise quantification of the risks associated with a military conflict that, although geographically concentrated, has global implications. Thus, two additional scenarios are considered, estimating the direct impact of the evolution of oil prices on GDP and inflation.

Scenario 1: between two and three months of conflict

Under this assumption, the Brent barrel would be set above 80 dollars on average during the first quarter of 2026, normalizing progressively from the second quarter. GDP growth in 2026 would be reduced by 0.3 percentage points, standing at 2%, and inflation would increase by 0.5 p.p. in 2026, although this effect would be corrected in 2027.

Scenario 2: prolonged conflict

If hostilities were to prolong, the conflict becomes entrenched, and the price of crude oil is above 90 dollars during 2026, GDP would grow by 1.6% in both 2026 and 2027; 0.7 and 0.4 percentage points less, respectively, compared to the baseline scenario. Inflation could rise to an average of 4% in 2026, which would erode the purchasing power of households and business profitability.

Global Context

The direct confrontation between Iran and the coalition formed by Israel and the United States has destabilized the transit of ships through the Strait of Hormuz, which is not only a mandatory passage for 20% of the world’s crude oil and 25% of liquefied natural gas (LNG), but is also a main artery for the export of nitrogenous and phosphated fertilizers produced in the Persian Gulf region (representing approximately 15-20% of the global supply of these compounds).

As a consequence of this situation, during the first days of the conflict there has been a significant increase in the prices of these raw materials, mainly due to the rise in insurance premiums for ships and their cargo. These policies have gone from representing a residual fraction of the cost of the cargo to accounting for a very significant percentage of the total value of the ship for each transit. Additionally, there is the diversion of routes caused by this situation, which implies an additional cost in the transportation of many goods.