2026 will be a turning point for the EU economy, according to the spring forecasts just released by the European Commission. These forecasts fundamentally point to lower economic activity, due to the conflict in the Middle East, which is reigniting inflation and shaking economic confidence.

Before the war against Iran began in February 2026, it was expected that the EU economy would continue to grow at a moderate pace along with a new decrease in inflation. However, since the outbreak of the conflict, inflation began to rise, driven by a sharp increase in the prices of energy commodities. The situation is expected to improve slightly in 2027 if tensions in energy markets decrease.

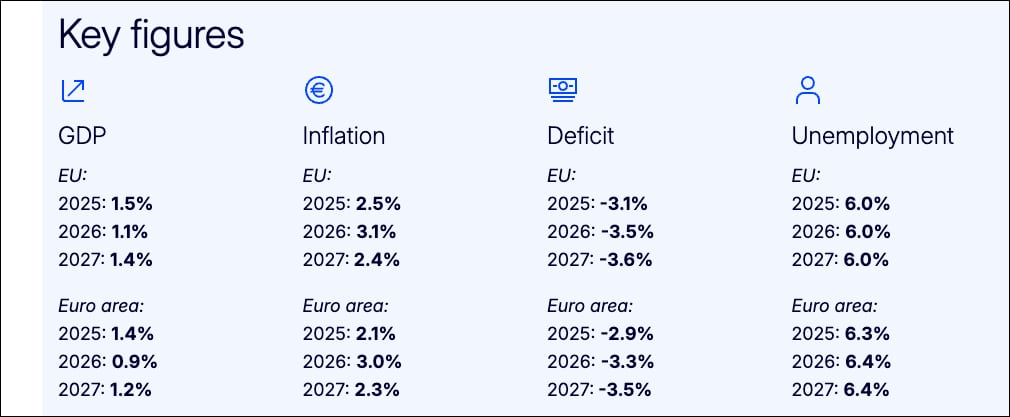

According to data provided by the European Commission, after reaching 1.5% in 2025, GDP growth in the EU is now expected to slow to 1.1% in 2026, which represents a downward revision of 0.3 percentage points compared to the autumn economic forecasts of 2025 (1.4%). GDP growth is expected to reach 1.4% in 2027.

Inflation in the EU is expected to reach 3.1% in 2026 – one percentage point higher than previously expected – and to drop back to 2.4% in 2027. In the euro area, inflation is also revised upwards, to 3.0% in 2026 and 2.3% in 2027, compared to the autumn forecasts, which were 1.9% and 2.0%, respectively.

With the onset of the conflict, consumer confidence fell to its lowest level in 40 months, in a context of growing fear of rising inflation and job losses. However, consumption is expected to remain the main driver of growth. Business investment is also expected to be limited by tightening financing conditions, reduced profits, and increased uncertainty. The weakening of external demand is also weighing on export growth.

The EU’s investment in energy resilience, especially after Russia’s large-scale invasion of Ukraine, is paying off. The push towards supply diversification, decarbonization, and reducing energy consumption has put the EU economy in a better position to face the current crisis.

The public administrations’ deficit in the EU is expected to increase from 3.1% of GDP in 2025 to 3.6% by 2027, as a consequence of the moderation of economic activity, rising interest spending, measures to cushion the impact of rising energy prices on vulnerable households and businesses, and increased defense spending. Public investment in the EU is expected to stabilize at high levels in 2027, despite the end of disbursements from the Recovery and Resilience Facility.

The main risk surrounding the forecasts relates to the duration of the conflict in the Middle East and its repercussions on global energy markets. Given the unusually high degree of uncertainty, the baseline forecast is complemented by an alternative scenario that assumes more prolonged disruptions. In this second assumption, energy commodity prices are expected to rise significantly above the baseline futures curves, peaking at the end of 2026 before gradually realigning by the end of 2027.

These forecasts are based on technical assumptions for exchange rates, interest rates, and commodity prices, with a reference date of April 29. Regarding other data considered, including hypotheses about public policies, these forecasts take into account information obtained up to and including May 4. The projections are based on the assumption that there will be no changes in policies unless measures are credibly adopted or announced and specified in sufficient detail.

The forecasts include two special sections dedicated to the reduction of energy consumption in the EU over the last three decades and to the gap in AI adoption. Through a series of boxes, the responses of macroeconomic policy to energy disruptions, manufacturers’ strategies in the face of trade tensions and disruptions, the current flexibility of labor markets, the links between gas and electricity prices, and national fiscal policy measures to address the energy price disruption of 2026 are also analyzed.

The European Commission publishes two comprehensive forecasts each year (spring and autumn), covering a wide range of economic indicators valid for all EU member states, candidate countries, EFTA countries, and other major advanced and emerging market economies. You can view the full report at this link.